The Lobito Corridor

The flagship 'highway for critical minerals.' Marketed as the West's answer to Belt and Road — resuscitated under PGII — but still prioritises evacuating unprocessed cobalt and copper for EU and US industrial demand.

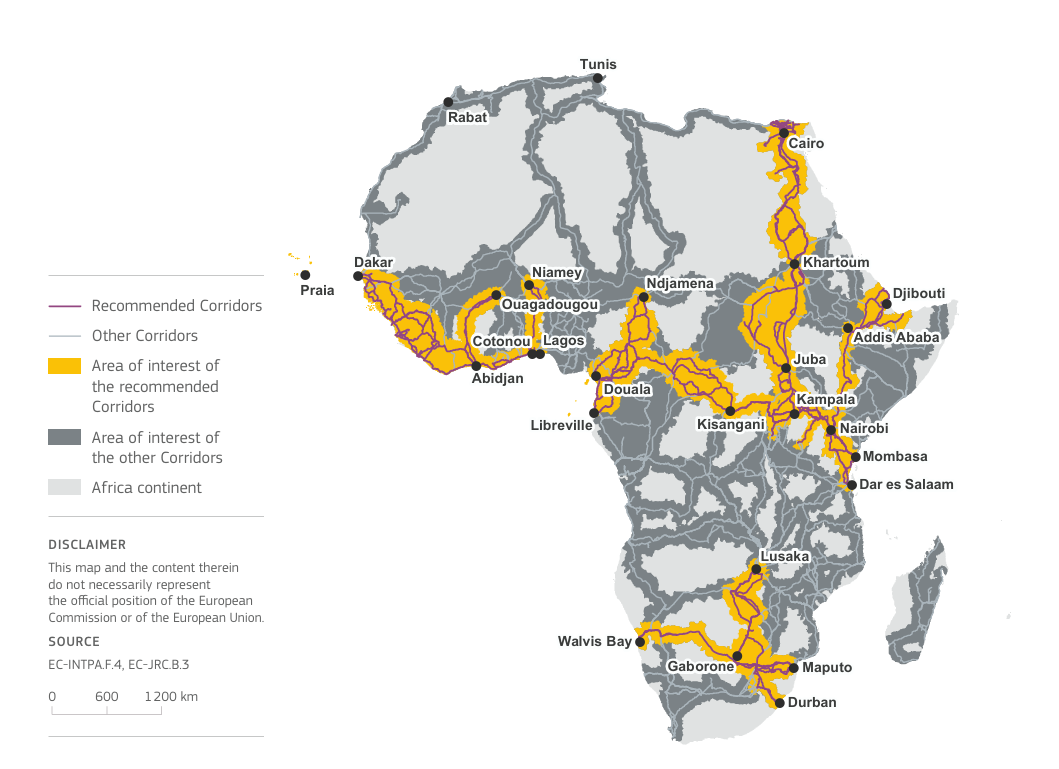

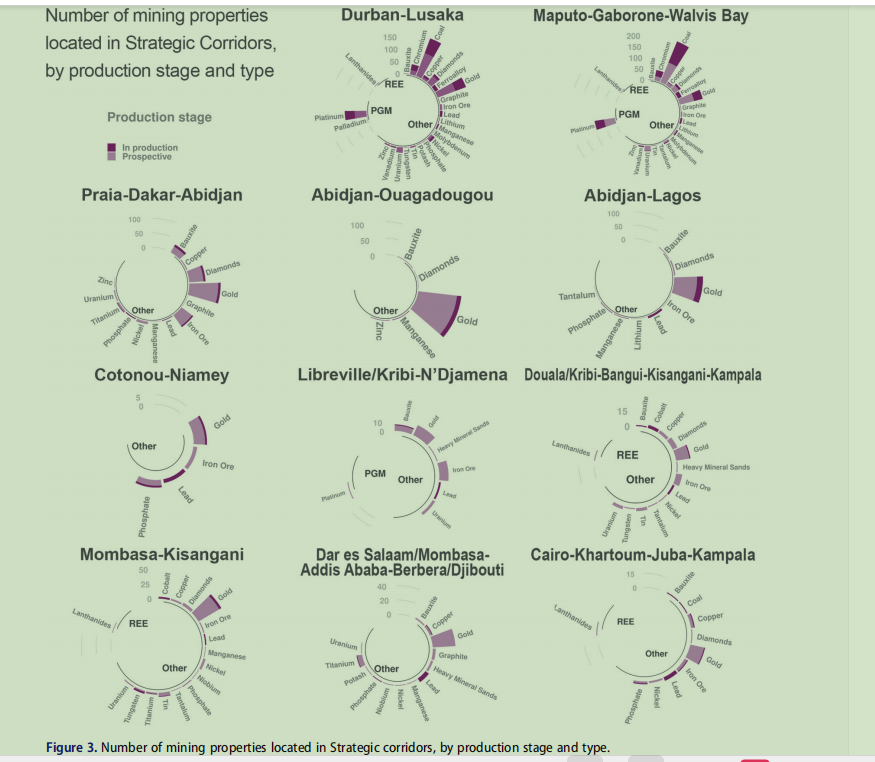

To illustrate the EU's interest in creating 'highways for critical minerals' to secure its demand, it is worth zooming in on the Lobito Corridor — an infrastructure corridor now supported by the Global Gateway connecting the DRC, Angola and Zambia. The Lobito Corridor links the mining areas of Katanga province in the DRC, home to more than 50 per cent of the world's cobalt reserves, while also passing the Copperbelt region in Zambia. International mining companies dominate these resource-rich regions. Historically, this corridor was one of the busiest transportation routes in southern and central Africa.

Regional efforts to revive the Lobito Corridor produced limited results. The project was resuscitated in late 2023 under the United States Partnership for Global Infrastructure and Investment (PGII), a G7 initiative conceived in the context of responding to China's Belt and Road investments in Africa. The corridor consists of a railway connection between Angola, the DRC and Zambia mainly to secure good access to raw materials. Under PGII, the governments of Angola, Zambia and the DRC are upgrading the corridor with support from the US, the Africa Finance Corporation and the African Development Bank.

The EU has signed a Memorandum of Understanding on the Lobito Corridor with the DRC and Zambia in cooperation with the US and other partners, and bilateral MoUs with the DRC and Zambia on raw-material value chains. G7 partners also signed an MoU with corridor partners during the first Global Gateway Forum in October 2023. Prominent investors with concessions include Trafigura, Mota-Engil and Vecturis.

US officials estimate the project will cost more than USD 1 billion. A breakdown of concessional financing from donors including the EU, host-government contributions, and private finance to be mobilised is not publicly available. Global Gateway's involvement is rooted in the EU's partnership with the G7's PGII: bringing projects to G7-based investors and commercial partners such as CitiGroup, rather than fostering local value and sustainable development for host countries. Privatised infrastructure models that compel Global South citizens and governments to pay expensive user fees offer not development investment but extractive rent.