Sharing the continent one more time

The EU Team Europe's 11 Global Gateway Strategic Corridors sinking Africa into a $724B debt

What European leaders have said about Global Gateway

Global Gateway does not bring new financial means – there is no additional money when it comes to the EU level,

"There's no new money (in the Global Gateway). And I've always held the view that if there's no new money, there's no new policy. This is a communications exercise. It's a strategy to put together what was already going to happen and present it as something new. And if our partners are tricked by this, then more fool them."

"It was never clear what was additional about Global Gateway. It draws heavily on existing programmes and initiatives that would have moved forward even if Global Gateway did not exist. It was sold as a viable alternative to China's Belt and Road Initiative (BRI), an alternative that was driven by values, like transparency and sustainability. It has not gone beyond just words."

"European Union is good at financing roads, but it does not make sense for Europe to build a perfect road between a Chinese-owned copper mine and a Chinese-owned harbor."

What is the Global Gateway — Myth vs Truth

The Myth

Launched in 2021, the European Union and its member states initially positioned the Global Gateway as a "joint Western alternative" to counterbalance China's Belt and Road Initiative's (BRI) growing influence.

But this approach was quietly dropped in 2025 when it became clear that comparing the GG to China's BRI was incorrect.

While the Global Gateway has adopted the Chinese BRI strategy of using the initiative to give contracts to its own corporations, the point of departure is that the BRI is a real fund that had by 2025 committed over $1T in investments, while the GG, while valued at slightly over $317B, is a mix of loans and loan guarantees (primarily to European corporations) to be paid back directly by the receiving governments and through Public Private Partnerships.

According to the EU, the global gateway is an excellent offering that should make Africa and the rest of developing "partner" countries extremely grateful.

France, under whose EU Presidency the GG was launched, describes it as "an initiative that contributes to the development of emerging market and developing countries".

The European Commission praises the Global Gateway as the best thing that ever happened to its partners.

It refers to the Global Gateway a new European strategy to boost smart, clean and secure links in digital, energy and transport sectors and to strengthen health, education and research systems across the world.

They go on to state that the Global Gateway "seeks a transformational impact with a focus on smart investments in quality infrastructure, respecting the highest social and environmental standards, in line with the EU's interests and values: rule of law, human rights and international norms and standards."

The Global Gateway even lists a set of "values and Principles", for which it has appointed a civil society advisory board to oversight — democratic values and high standards, good governance and transparency, equal partnerships, green and clean, security focused and catalyzing the private sector.

The Truth

A 2020 report by DIE, the German Institute for Development Policy, gives an open and candid assessment of what has become known as the EU's public face and private life.

What the EU and its member states promote in public and in its official documents is, according to the DIE, far from what they mean and do in practice.

DIE report shows that despite the EU insisting that there is no trade-off between its interests and those of…people living in the Global (majority) South, what it calls "principled pragmatism" in its 2016 Global Strategy), in practice this is not how Europe relates with Africa.

Instead Europe's dealing with Africa is characterized by a continuous trend of instrumentalizing EU development aid for the purposes of pursuing European economic and security interests, and "protection" against real or perceived "threats" emerging from neighbouring countries, in particular.

The Global Gateway has taken this trend to its highest level.

While on paper the Global Gateway is projected as partnership informed by Africa's needs coming out of a so-called Joint AU-EU Strategy for Africa and Agenda 2063, the global gateway is a tool that will firmly secure European grip on Africa through a combination of skewed long term extraction contracts, unsustainable debt, and energy and infrastructures that are deliberately structured to serve European industries.

History of the Global Gateway — Dividing Africa to Corridors

In 2022, the European Union officially launched the Global Gateway, announcing an investment package of $346.03B, $173.017 of which was earmarked for Africa between 2022 and 2027.

But the announcement was misleading, at least in the case of Africa. This is because while the Global Gateway was promoted as the EU's contribution to the G7's Partnership for Global Investment In Infrastructure (PGII), to fully understand how Europe arrived at the Global Gateway one needs to go back to the mapping of the African continent along its resource paths under an initiative known as Corridors and Urban Systems in Africa — CUSA.

CUSA Corridors: Preparing Africa For Extraction

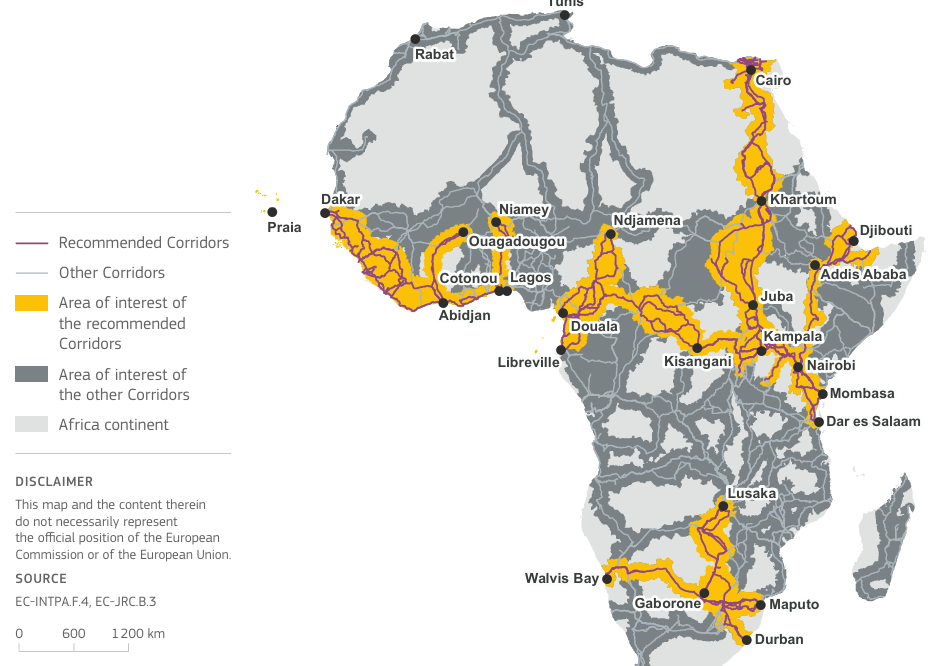

The history of the Global Gateway in Africa begins with the outcome of a mapping of strategic corridors in Africa by the European Commission, under a project known as CUSA.

The Mapping, carried out in two phases, narrowed down a list of 11 passage ways from an initial identified potential of 55.

These eleven were based on four policy scenarios:

But a closer look reveals, especially when considered against the 140 indicators, that Europe's interests in these corridors were on four main areas — digital sector, energy (including Green Hydrogen), transport and logistics and health (especially vaccine manufacture and the pharmaceutical industry). They were also areas with the needed human capital to help in the exploitation of resources, albeit with small policy changes in education and research.

In order to identify the countries that met the requirements of extractive corridors, one hundred and forty (140) quantitative indicators were used, resulting in the initial fifty five (55) Strategic Corridors.

From the 55 a shortlist of 11 Strategic Corridors was identified — four in West Africa, two in Central, two in East and two in Southern Africa, as well as one in North East Africa.

Some of these indicators are very telling:

1 How much the region trades with the EU in absolute and relative EU Export & Import.

2 Estimated availability of mineral resources, expressed in number of mining locations.

3 Percentage of the corridor that is projected to be used for agriculture, as crops or permanent crops, in the year 2050.

4 World Bank Vs Chinese Financing of projects in the corridor between 2004-2014.

5 Connection to EU Ports — Number of distinct connections involving any specific container port within the corridor and any container port in the EU.

6 Number of events classified as Violent events, Demonstrations or Non-Violent Actions, which have taken place from 2015 until January 2021.

Below is a mapping of the 11 Corridors based on their extractive potential:

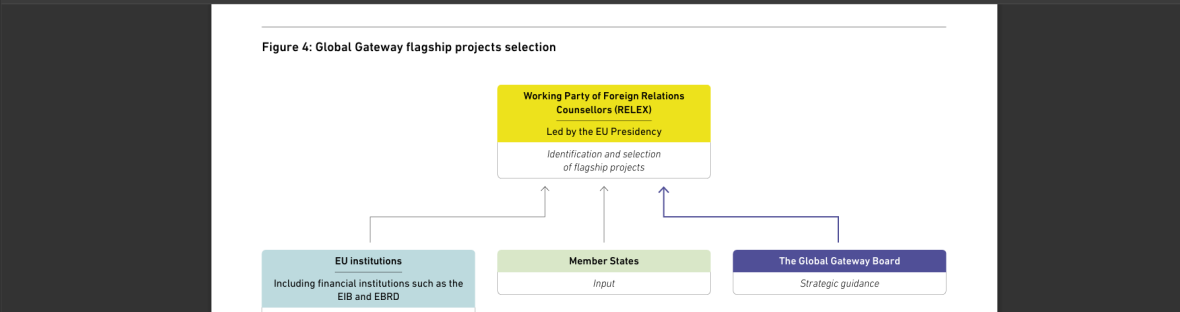

One of the key things to note is that the Corridors were evaluated against a set of broad criteria jointly defined by EU Department for International Partnership (DG INTPA) and JRC, with no input from, or awareness by, Africa.

It was, once again, a joint European partition, this time under what has become known as the Team Europe initiative.

And the EU does not hide its reasons for this partitioning. The CUSA Report makes it clear as follows:

Africa – the EU's close neighbour… is a continent full of opportunity and potential for cooperation and for business… with private consumption expected to reach € 2 trillion annually by 2025. The EU should therefore make the most of the political, economic and investment opportunities that these changes will bring… through international partnerships that uphold and promote European values and interests. A fresh start on migration would also help stop smugglers and bring a stronger commitment to resettlement, as well as pathways for legal migration to help bringing in the EU the people with the skills and talents the EU needs.

The 11 recommended corridors were formally unveiled in the conclusions of the EU-African Union Summit on 17th–18th February 2022.

Shortly thereafter, the first Global Summit saw the beginning of signing of contracts, MoUs and agreements, most of which were related to realigning of old agreements with EU member states…. and that is how the Global Gateway began to unfold.

Piggybacking on PGII — CUSA was anchored on the G7 Agenda

While CUSA provided the justification for the division of the continent, the G7 summit provided the Platform from which the financing and diplomatic negotiations would be actualized.

The EU's strategic corridors were invariably going to get in the way of other interests, key being China, the US, Italy (which had already begun to chart its own path away from the EU) and Japan.

In 2022 the G7 launched the Partnership for Global Infrastructure and Investment (PGII). PGII is the repackaged version of the Build Back Better World (B3W) initiative which President Biden announced at the 47th G7 summit in the United Kingdom.

It was billed as "a shared commitment to advance public and private investments in sustainable, inclusive, resilient and quality infrastructure...aiming to mobilize up to USD 600 billion by 2027 in order to narrow the infrastructure investment gap in partner countries."

PGII quickly became the collective vehicle for most G7 previously independent initiatives — EU's Global Gateway, Italy's Mattei Plan, Japan's Green Growth Initiative with Africa (GGIA) and US's commitment.

Publicly the PGII is billed as a $600B G7 Investment initiative; the actual strategy was not about flow of Foreign Direct Investments (FDIs).

Instead the entire set of initiatives is intended as a series of loans and loan guarantees.

The strategy is to mobilize private sector investment under Public Private Partnerships (PPPs) with target countries, as well as loans from these countries and through financial institutions, a model first presented by the US as its sole strategy for raising funds for PGII.

The European Union then officially launched the Global Gateway, announcing an investment package of $346.03B, $173.017 of which was earmarked for Africa between 2022 and 2027.

In reality, however, all the G7 actors — US, EU, Italy, and Japan — were not putting in any new resources. They were simply going to repackage existing loans and guarantees, with an additional set of loan facilities made available through multilateral and Development Finance Institutions, including the World Bank, European Investment Bank and the 14 European DFIs.

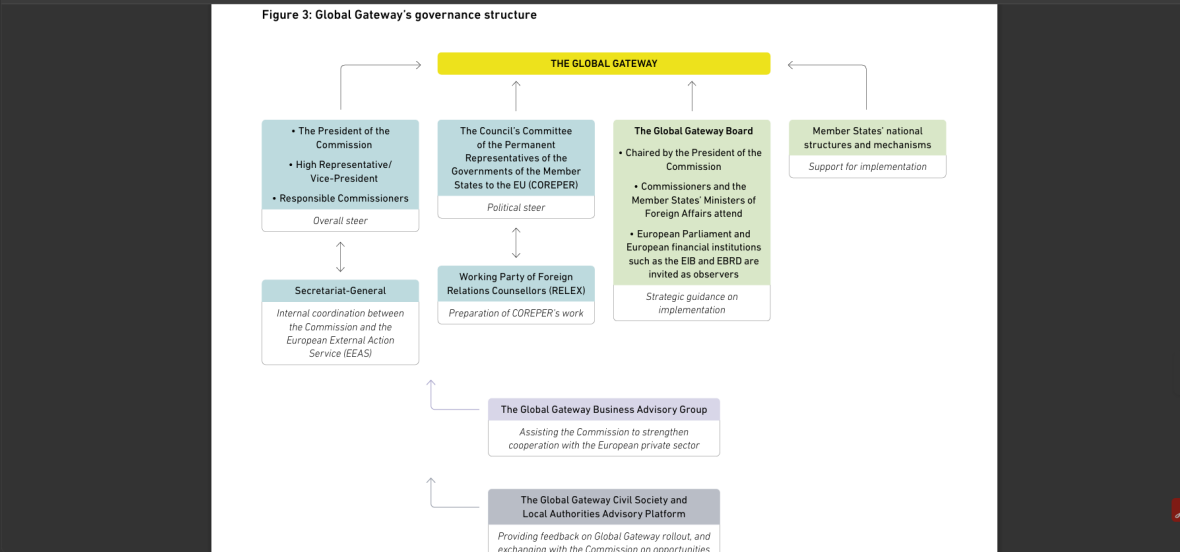

From PGII to Team Europe: The EU's Financial and Political Force for the Global Gateway

In order to take the full advantage of different economic and geopolitical powers that individual EU member states have over Africa, a joint approach was adopted, known as Team Europe.

Team Europe was first adopted by the EU as a collective response to the COVID-19 pandemic and the need to combine EU institutions and EU member states joint efforts.

Team Europe is made up of the following:

- 1All EU Member States

- 2European Commission

- 3All Development and Investment Banks, including European Bank for Reconstruction and Development, European Investment Bank and the 14 European Development Financial Institutions.

- 4Leading European Multinationals in the core CUSA corridors.

- 5Selected Development agencies such as the German GIZ.

Team Europe brings together the entire political, financial and diplomatic muscles of the EU to create an impenetrable Wall that makes sure that negotiations are coordinated, projects shared among members, risks spread and most importantly bickering over project control remains internal within the Union Governance structures.

In short it addresses one concern that has plagued the EU for decades — internal competition over resources in countries of extraction.

What this means is that while individual African countries may be negotiating as a country on a single Global Gateway project, Europe is coming with the full diplomatic, political and financial muscle of 27 member states, 14 Development Financial Institutions, entire European Commission machinery, European External Action Services (EEAS), the European Investment Banks, and all the multilateral institutions that receive significant financing from the EU and its members such as Africa Development Bank and the World Bank.

In short, you have a set of tiny and economically weak countries, some with economies as small as $27B (Mozambique) negotiating with the political, diplomatic and economic muscle of a European juggernaut of $21 trillion in nominal GDP and purchasing power parity (PPP) of $43.8 trillion!

Add to this the diplomatic muscle of powerful countries such as France, Belgium and Germany, and the entire machinery of the European Commission, which has its own budget and diplomatic representation across nearly all of Africa, and you immediately see that this is framed as an engagement that Africa cannot win.

Not with a disjointed Africa Union that offers no buffer in any form of negotiations or resistance.

Why the Global Gateway is attractive to European corporations

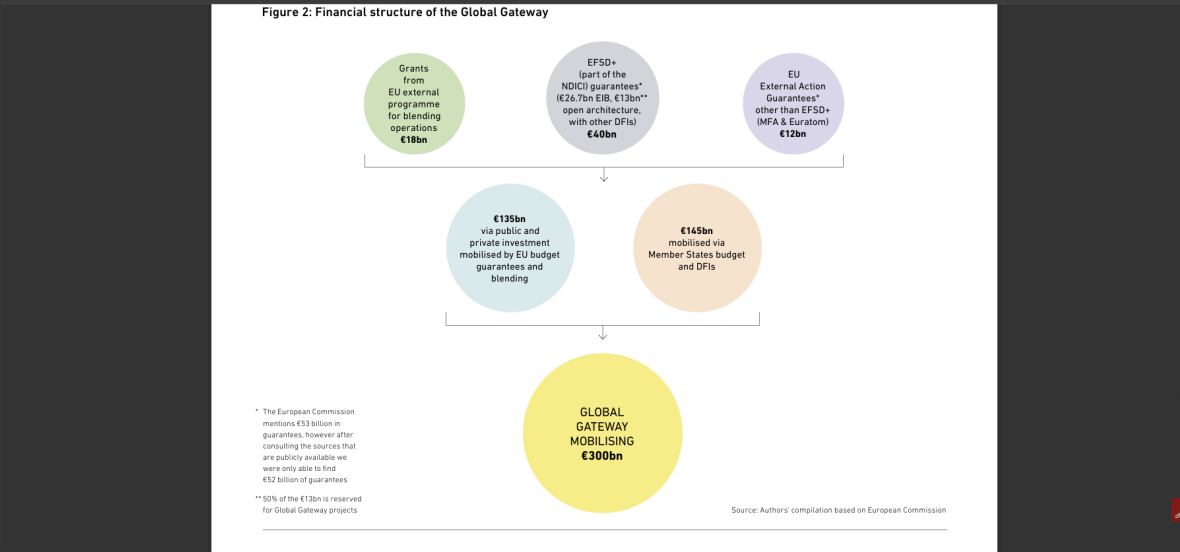

First, the bulk of the Funding for GG projects (close to 89%) is coming from EIB, the 14 DFIs and directly from the individual member states, not from the private sector.

Secondly the European Commission is offering additional grants to the DFIs, the EIB and member states for any projects that are classified and approved under the GG. The amount is little (about EUR 20B-60B), but the attractive part is that the funding serves two purposes — it offers risk guarantees (what we sometimes classify under blended finance), and technical support that enables both the EIB and the DFIs to carry out technical reviews and support that would have otherwise rendered some European corporations unable to take advantage of any of the GG projects.

It is important to understand this funding model, because it is the reason that has made the GG very popular with literally all the member states.

Finally the fact that the funding model creates a near level play-field for corporations across entire Europe, and the fact that it allows for projects to be carried out jointly by corporations from multiple member states, is extremely attractive and is the main selling point for the GG.

But this attractiveness is also the reason why the GG will be so devastating to economies across Africa.

First the idea of making the GG benefit local economies outside of the member states is not going to be compatible with the core reason and core motivation for the GG.

The EU claims that there are clear regulations that have created a system for "open tendering" that allows any company around the world to compete for any EU project according to the World Bank, Local and EU regulations.

But that is false.

First the guarantees and technical support being offered are primarily to European corporations, giving them a significant headstart in any GG initiative.

Secondly, as has been noted in ongoing GG projects, the primary condition is that, contrary to the EU claiming compliance to open tendering rules, the projects are led and executed by European corporations.

Finally, currently the entire Global Gateway Business Advisory Board, the group that designs and selects GG projects, is made up purely of European corporations.

They are the only ones with access to all information on GG projects and their financing arrangements.

Industrialization and Project Selection

There are some very good proposals around how the GG can help industrialize the continent and build up local production and value chain.

This is a very good demand and in fact it alludes to the other proposals in the document — responding to African market realities and build regional competitiveness, a deeper assessment of local value chains, Knowledge and skill transfers, as well as SME mentorship programmes, better connection with Africa's emerging business ecosystems and SMEs.

There is only one problem.

This is NOT the reason the GG was established.

If it were so then the EU would have, in parallel, allowed other discussions around Technology Transfer, Intellectual Property, tariff and Non tariff barriers, and deliberate partnerships and funding models that are available to both European and partner corporations.

Instead the EU has been pushing for Economic Partnership Agreements (EPAs), the Samoa Agreement and other market rules that are completely consistent with its push for dominance, not capacity support. And it has ensured that any discussions around the issues mentioned above are completely removed from the GG Dialogue structures. The recent GG Summit was a clear indication that there is absolutely no intention to broaden the discussions to how investments can add direct value to partner countries.

Project selections are therefore based not on their value to partner countries (even though this is the rhetoric you will hear literally everywhere), but on the ability to ensure they entrench existing rules of play and do not allow for discussions on areas deemed to have an impact on Europe's global competitiveness (read dominance).

Ownership of the GG projects: Project Selection

One of the notable issues around the GG is the insistence by the EU that every project is a result of long term consultations with partner governments.

And any attempts to try and demonstrate that it is the contrary is met with resistance.

The idea of "consultations with partner countries" is not just about the EU meeting legal requirements, it is also about demonstrating legitimacy among partner states and its citizens.

This is not how the GG works.

The EU will tell you that the projects are selected in consultations with "partner countries" and that they are all aligned to the six core GG Principles and values —

In practice, however, this is how it works.

First, all projects should align to the mapping of the selected 11 Strategic Corridors under CUSA.

This is important because the core outcome of the Global Gateway is to take full control of resources and related logistics needed to move these resources to their destination — Europe.

Having met this requirement, members of Team Europe follow the following methodology.

European Member States

Member states come up with their own projects in respective countries of interest. These are then negotiated with politicians in partner countries.

Yes, you heard that right.

There is not a single Global Gateway project that has been negotiated with the full involvement of citizens or legislative assemblies in these partner countries.

Once the negotiations are concluded with the executive, often under secrecy and with no clarity as to the motivations given to the politicians, they go straight to Government organs, which in nearly all cases across Africa, exist to serve the executive.

Once an agreement has been reached, projects are then presented to the Global Gateway Governance Board, who then through a process of negotiations decide how it can be shared out to benefit other member states.

Development and other Financial Institutions

The European Commission, through its Directorate of International Partnership and the Diplomatic Service (External Action) actively engage with partner states.

For the DFIs and the EIB, they are required to continue to "actively solicit" projects in their respective areas of operations. The terms of the loans can be very deceptive — 40 year repayment periods, and low interest that comes with long grace period.

And that is the hook.

Deceptive long term loans with deceptive terms for projects that the countries do not need.

Just the kind of conditions that make politicians quickly embrace projects that tie their countries to unending debt.

The end result is that literally ALL projects are negotiated with Politicians.

We have reviewed all GG projects across Africa (and there are about 300) and there is not a single one, including very large infrastructure projects, that have been debated and approved by respective Parliaments or details shared with citizens.

By restricting discussions to politicians, the EU can claim "ownership" while knowing very well that many of the projects actually violate rules of partner countries such as Kenya that require public participation in large scale projects.

Again this is deliberate to try and increase the speed of uptake and decrease the levels of scrutiny.

Engagement with AU and AU Agencies

The entire strategy of the EU's engagement with Africa is premised in what is known as "Joint Partnership".

This means that the EU is, by virtue of its structure and values, required to treat third countries as equal partners.

But there are problems with this engagement at three levels:

First the assumption that these countries are operating under the similar rules that allows for equality is a fallacy. The EU and its member states has controlling power over multilateral institutions and spaces that are supposed to ensure equality. It has, alongside its members, control over the World Bank, the WTO, the IMF and the core rating agencies that collectively define the financial rules of engagement.

Secondly, Africa's combined GDP is smaller than Germany, a single member of the EU. It is not feasible to have a partnership of equals.

Beyond these dynamics the EU as an institution has multiple independent engagements that makes this impossible.

To begin with member states have their own rules that are informed by their own interests and political persuasions.

Then the Development Financial institutions are driven by the interests of their respective member states. This is the same driver of different corporate interests.

The European Commission also has a direct engagement, creating not just a serious overload for third party countries, but conflicting interests that make it difficult for any coherent policy that informs a collective EU-wide approach.

The Global Gateway suffers significantly from these differences.

And that is why it is impossible to evaluate various projects through a set of Global Gateway values.

A classic case is the recently released joint EU-Africa 2030 Vision Progress Report. The report even opens by stating thus:

The Global Gateway Africa-Europe Investment Package, endorsed at the summit, is on track with its EUR 150 billion investment target by 2027, with 95 Team Europe Initiatives (TEIs) already developed for Africa. Key flagship projects, particularly in Africa, are advancing, with visible results in areas requiring technical and financial arrangements. Civil society and youth engagement are also emphasized as crucial drivers for success.

This report reflects an attempt to project the engagement as being about the society, when in reality each individual project relies on the rules set by the countries and financial institutions driving the respective projects.

As at January 2026, there is no civic engagement in any project outside of the framework that has informed traditional relationships.

The European Commission engages with Civic actors, private sector and governments directly through its department for International Partnership, INTPA.

This happens primarily at the European Commission Offices in Belgium.

The delegations engage through their diplomatic channels under the European External Action Services.

The various financial institutions relate with member states as "clients" and are therefore not open to making details of any relationship available to the public.

Individual member states have continued to use their own embassies to engage directly, with no desire to include public participation.

The consultation with the AfDB is in financing, not in project identification.

The same applies to consultations with Afrexim Bank.

And no, there are no consultations with civil society in any country, except in Kenya where a civic group is in the formative stages, five years after GG.

The hydrogen myth

The hype around hydrogen risks increasing reliance on fossil gas. While small quantities of truly renewable hydrogen may be suitable for local heat and electricity generation or for a limited scope of industrial activities that are difficult to decarbonise, they will represent only a fraction of the current fossil gas consumption. So far, renewables-based hydrogen production has been minimal. According to Corporate Europe Observatory, in 2022 less than 0.1 per cent of global hydrogen was produced from renewable electricity. It remains an expensive, inefficient, and energy-intensive solution, supporting a centralised fossil fuel-based energy model to the benefit of a handful of large companies.

At the same time, hydrogen projects risk encroaching upon local affordable renewable energy availability and risk having negative human-rights, social, and environmental impacts due to a large resource demand — land, renewable energy, or water. Greenwashing is also a risk in 'hydrogen-ready' infrastructure investments, as there are various types of hydrogen, including those based on nuclear or fossil gas.

The emphasis on green hydrogen projects, influenced by the EU Global Gateway, raises fears of exploitation and the creation of sacrifice zones. There is apprehension that our renewable energy resources might be used for the benefit of the Global North, echoing historical patterns of resource extraction and colonisation that prioritise profit over our citizens' needs.

Overall, most investment in the electricity supply chain concentrates on utility-scale infrastructure, with generation attracting around two-thirds of investment, one-tenth for transmission networks, and the remainder for distribution. Within this chain, European companies benefit from engineering, procurement and construction contracts and power-purchase agreements. Many renewable projects of the Global Gateway are proposed as Public-Private Partnerships — such as solar plants in Benin or Côte d'Ivoire — and reflect the Gateway's approach of creating opportunities to tap into EU companies' competitive advantages.

Characteristics of the Global Gateway Projects

Negotiations Black Box

Projects are negotiated individually between "Team Europe" (a mix of the EU Commission, member states, and the EIB) and partner country politicians. These negotiations are often confidential until a final agreement is reached, creating a "black box" effect that limits scrutiny during the development phase.

Political Sensitivity and Diplomatic Narrative

The EU is cautious about openly framing the Gateway as financial competition with China, preferring to present it as a collaborative, values-based offer. This diplomatic posture discourages explicit financial comparisons and contributes to the opacity.

Illusory Ownership and Restricted Consultations

The EU insists that every project results from consultations with partner governments to demonstrate local ownership. In practice, these consultations are almost exclusively conducted with politicians. A review of approximately 300 Global Gateway projects in Africa reveals that not a single one has been debated or approved by respective national parliaments, nor have details been shared with citizens for public participation, despite this being a legal requirement in countries like Kenya. By restricting discussions to the executive branch, the EU expedites project uptake while minimizing democratic scrutiny.

Euro-centric Project Selection

Project selection is not primarily driven by their value for industrializing partner countries or building local capacity. Instead, selections are made to entrench existing trade and investment rules that protect Europe's global competitiveness. The EU has deliberately excluded parallel discussions on technology transfer, intellectual property, and tariff barriers from the Global Gateway dialogue structures. The recent Global Gateway Summit confirmed there is no intention to broaden discussions to how investments can directly add value to partner economies beyond infrastructure development.

Impact of Global Gateway — A Look at the impact of the Lobito Corridor

Disregard for Peace, Human Rights and The Environment

The Global Gateway does not draw a clear distinction between the EU's infrastructure investments and the prestige projects of autocrats.

This is what The Global Gateway has done with projects in Uganda, DRC, Rwanda, Mozambique, CAR, Morocco, Tunisia and recently an authoritarian leadership Kenya, where the Global Gateway has pitched the bulk of its so called "Sustainable Aviation Fuel" and "Green energy" projects.

In fact when one looks at Global Gateway initiatives you can see that the least of European concerns in their choice of projects is stability of those countries. It is almost as if we are back to the 80s and 90s when instability meant more risks, but also with extremely high returns.

Infrastructure projects that ignore socio-environmental impact assessments not only lead to environmental devastation, but also fuel economic and political grievances. Investments in authoritarian countries (as the World Bank did in 1991 when it gave loans to a dictator in Somalia) serve to stabilise regimes, and it is more likely that human rights and environmental concerns will be sidelined before projects are abandoned and private capital is lost — *Europe's Global Gateway: A New Geostrategic Framework for Development Policy?*

Global Gateway frequently favors European commercial interests and does not place a major emphasis on addressing inequities in partner nations, thereby undermining its effectiveness and image in the Middle East.

Central Africa: The Lobito Corridor — An "Economic Corridor" or an "Extraction Corridor"?

The flagship GG project involves the rehabilitating the 1,300 km Lobito railway from Angola through the DRC to Zambia.

The project is overwhelmingly focused on exporting raw minerals. While the corridor promises local development, its primary economic logic is to drastically reduce transport costs for multinational mining conglomerates extracting copper and cobalt, thus boosting their profits.

The DRC and Zambia accrue more debt for the infrastructure while still being locked out of the lucrative stages of the battery supply chain. This directly mirrors the 20th-century colonial infrastructure model.

2. West Africa: The Dakar-Diamniadio Toll Highway — Debt-Financed Elitism

**The Project:** A toll highway and rail link in Senegal, financed by AFD and EIB, built by French company Eiffage.

**Existing Analysis:** The Senegalese Civil Society Forum on the Illicit Financial Flows (FOSCII) and other local NGOs have consistently critiqued such projects. Their analysis shows that the high toll fees (approximately €2 for a single journey) make it inaccessible for the vast majority of Senegalese, who rely on informal transport. A study by the African Development Bank (AfDB) itself has highlighted that a lack of affordable, integrated public transport is a primary constraint on urban productivity and poverty alleviation in cities like Dakar.

**Demonstrating the Fallacy — Project Selection:** The project was not born from a participatory urban mobility plan prioritizing the needs of the poor. Instead, it fits the classic "blended finance" model critiqued by Eurodad, where a large, visible, revenue-generating (via tolls) project is attractive to European public and private financiers, even if its developmental impact is narrow. It solves a problem for international business and the local elite, not the foundational mobility crisis for the populace.

3. North Africa: The Euro-African Digital Gateway — A Question of Digital Sovereignty

**The Project:** Undersea cables like the Google-backed "Equiano" and the EU-supported "Medusa" linking Europe to Africa.

**Existing Analysis:** Research from the World Wide Web Foundation and Africa-focused digital rights groups like Collaboration on International ICT Policy for East and Southern Africa (CIPESA) has long warned of "digital colonialism." Their work shows that while new cables increase bandwidth, the control of data, internet exchange points (IXPs), and cloud infrastructure remains largely with a few non-African tech giants and telecoms. This recreates a "hub-and-spoke" model where intra-African data traffic is often routed through Europe, increasing costs and undermining sovereignty.

**Demonstrating the Fallacy — Ultimate Beneficiaries:** As per CIPESA's analysis, the primary beneficiaries are companies like Google, which can sell more cloud and connectivity services, and European telcos. The GG's digital strategy, by focusing on physical infrastructure without parallel, massive investment in local digital ecosystems (e.g., funding African startups, strengthening local IXPs, building robust data protection authorities), reinforces this dependency. Africa gets into debt to deepen a digital ecosystem it does not control.

4. Eastern Africa: "Sustainable" Agriculture — Locking into Export Dependency

**The Project:** GG funds promoting "climate-smart" agriculture for export crops in countries like Kenya and Ethiopia.

**Existing Analysis:** The Institute for Agriculture and Trade Policy (IATP) has extensively documented how such "sustainable" labels often mask the consolidation of global agri-food chains. Their research shows that smallholder farmers are locked into volatile contracts with European supermarkets, bearing all the risks of climate and price shocks. This model actively undermines food sovereignty, a concept championed by African food rights alliances like the Alliance for Food Sovereignty in Africa (AFSA).

**Demonstrating the Fallacy — Tied Aid & Policy Capture:** AFSA's position papers argue that such initiatives often come with "tied" conditions, promoting specific European-certified seeds and technologies, which displace resilient indigenous seed varieties and knowledge. The GG, in this context, functions as a vehicle for European agribusiness to capture African agricultural policy and production systems, orienting them away from self-sufficiency and towards serving European markets — a dynamic powerfully analyzed by researchers like Prof. Ian Scoones at the Institute of Development Studies.

Global Gateway and Multilateralism

The confluence of three factors enabled the creation of Global Gateway. First, the EU established this new instrument to counter China's role as a global infrastructure lender in Africa. Second, Global Gateway was possible through the shift to private investment in multilateral development financing.

The rise of China as a geopolitical power and the shift to private investment to finance development projects contributed.

The EU High Representative and the Commission jointly released the European Economic Security Strategy in June 2023, which identifies Global Gateway as one of the three pillars of the EU's economic security. This new strategy aims at protecting the EU's economic security, promoting the EU's competitiveness, and partnering with countries on similar de-risking paths which have common interests with the EU. Negotiating trade agreements, investing in sustainable development in the Global South, and securing links across the globe through Global Gateway are ways of achieving the partnering objective.

Global Gateway — EU's End Game

Internal documents reveal that the EU is seeking to address the following issues.

Change Policies of Third Countries

This is what the EU calls 360-degree approach.

Provide Finance and Loans

Then make sure that investment in hard infrastructure goes together with sectoral reforms and regulatory environment to provide long term favourable policy environment to European companies. A classic case is the Vaccine initiative. This is being used by the EU to "identify qualitative obstacles to scaling up the pharmaceutical sector" and develop academic cooperation, and link up businesses through a new Business Forum.

Target the minds of citizens, not governments

A brand, served by a new approach to strategic communication centred around campaigning to people rather than governments. A single Global Gateway brand and visual identity helps project an image of confidence, reliability and sustainability. The idea? Make the Global Gateway the new face of European Branding, and a regular fixture on the international scene on critical issues surrounding global connectivity. The new College should move to a full political campaigning approach through campaigns with local influencers in local languages making the connection between people's concerns and aspirations and the partnership that the EU brings. This also requires a serious investment in political engagement in partner countries backed up by investment missions with the private sector. It will also require an overhaul and professionalisation of the way the EU Delegations communicate.

Create a European Firepower

Team Europe means joining forces, pooling resources and combining expertise and tools. The firepower exists. Using its collective power at the EU and its Member States for instance account for 30% of all UN funding, 25% of the World Bank's capital, and 33% of the IMF's assets. Team Europe can also be an important visibility instrument.

Promote European Standard Abroad

Going forward, there remains significant potential that could be tapped into. The practice of Team Europe could serve more traditional channels of EU coordination, and enable louder EU representation where our voice remains subdued, in line with the Lisbon Treaty. Going beyond funding, it could also help structure our normative engagement and nurture a more strategic culture of cooperation. It should thereby be instrumental in promoting our core internal policies.

Ringfence Africa

The continent is rich in renewables (e.g. it hosts 60% of the world's best solar resources) and minerals (e.g. over 70% of the world's cobalt is produced in the Democratic Republic of the Congo), but it lacks investments (e.g. only 2% of global investments in clean energy are made in Africa), sufficient refining capacity, and is hugely exposed to climate change, despite contributing just 3% of global carbon emissions. To deliver on its geopolitical priorities, Europe needs Africa as much as Africa needs Europe. And to advance EU interests at the multilateral level, collaboration with African partners, representing about one-fourth of UN members, is key. Africa, conscious of its potential, is in the market for (non-exclusive) partnerships to pursue the objectives outlined in its African Union Agenda 2063. This translates into a battle of narratives and offers. Over the past years, a number of African countries, in particular in the Sahel, have decided to discontinue cooperation with the EU or some of its Member States.

Maximise impact

Show that the EU can deliver results by focusing on a limited number of Global Gateway flagships, which clearly showcase the impact of Global Gateway in Africa. These include actions (a) at national level, such as fostering vaccines production in Rwanda, Senegal, Ghana, and South Africa; developing sustainable raw materials value chains in Zambia, DRC and Rwanda; and advancing green hydrogen in Namibia and Mauritania; (b) at regional level, such as developing the Lobito Corridor in Angola, Zambia and DRC; and (c) at continental level, such as the EU support to the implementation of the African Continental Free Trade Agreement.

What the Global Gateway Means for Europe

With the economy now serving as the battleground for geopolitical competition, the Global Gateway has become the tool to resuscitate the European Economy.

The global economy grew 13-fold since 1950. The world is getting richer, but the way in which the cake is divided is changing. In 1990-2021, GDP per capita increased everywhere, with the biggest rise in Asia (over 200% increase) and the slowest in Sub Saharan Africa (+ 23%). EU: +46%. The EU's share of the world's economy is shrinking, from 34% in 1980 to 20% in 2022 (IMF). By 2030, the EU's share of the global economy could be around 12% (PwC). In contrast, Asia accounted for 22% of the world GDP in 1980, and 39%, today. By 2030, it could make up 60% of the world's GDP. Least Developed Countries (LDCs) today account for approximately 1% of world's GDP, roughly the same share as in the early 1970s. However, there were 25 members in the LDC category in 1971, and 46 today. GDP-per-capita in LDCs has gone down from 15% of world average to 10% of world average (UNCTAD).

What this means is that the opportunity remains in using resources from the LDCs to shore up economic growth in Europe.

Energy Dependencies

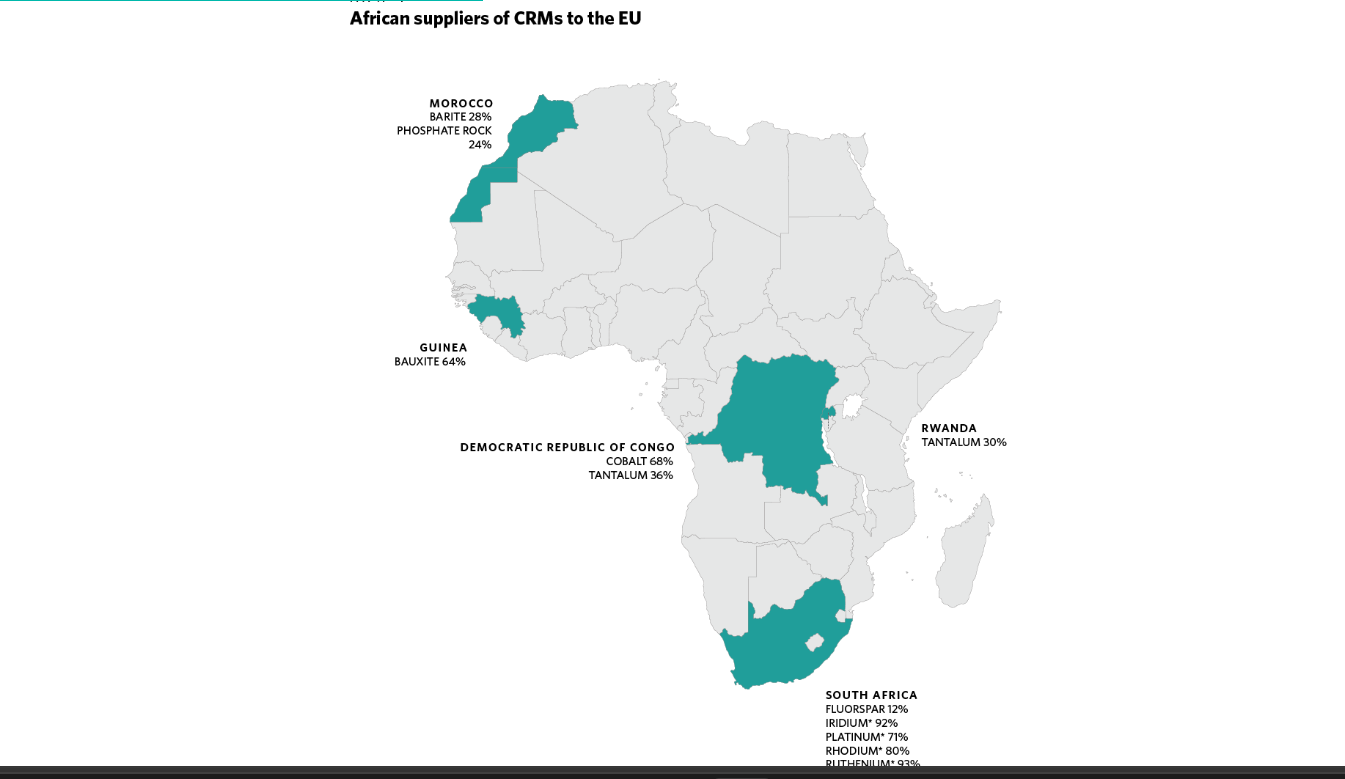

The EU is a net importer of energy (55% of energy used in 2021 was imported). The green and digital transitions should reduce EU reliance on fossil fuel producers but expose the EU to new dependencies. Nearly 90% of the processing and refining for manufacturing-grade critical raw materials is concentrated in China, with an even higher proportion for some materials such as Rare Earth Elements.

How GG benefits European Members

It unifies grants, blending and guarantees. This follows the adoption, in June 2021, of regulations on the Neighbourhood, Development and International Cooperation Instrument — Global Europe. It allows the EU to promote public and private investment worldwide through the European Fund for Sustainable Development Plus (EFSD+). In 2024, the EU opted to further align its programmes with the Global Gateway strategy.

It includes the reinforcement of investment envelopes, pooling provisioning of guarantees, related technical assistance, blending to fund mature and strategic projects, and the creation of envelopes for countries "in complex settings" to allow the EU to better calibrate its engagement.

How does Global Gateway Compare to China Road and Belt Initiative

A comparison of Global Gateway with the Chinese BRI project gives insights into volume and structure of the European initiative. First, the BRI operates on a much larger scale than the Global Gateway. While estimates of China's financial engagement in Africa vary, the Chinese Loans to Africa Database at Boston University's Global Development Policy Center reports that Chinese lenders made 1,188 loan commitments totalling $160 billion to African governments and state-owned enterprises already between 2000 and 2020. In comparison, the EU's Global Gateway aims to mobilize €150 billion for Africa between 2021 and 2027. However, China's investments in Africa are ongoing and expected to continue throughout this period. (Foretia 2024, 19) There are also calculations, that the BRI offered loans ranging from €200 billion to €400 billion, according to various estimates from the American Enterprise Institute and UNCTAD. (Tagliapietra 2023, 1327) This would clearly place the European Global Gateway Program in second place. Additionally, it must also be taken into consideration that, while the Global Gateway adds strategic focus and geopolitical intent (e.g., countering China's Belt and Road), its financial volume significantly overlaps with existing ODA commitments. Therefore, it is better understood as a reframing and consolidation of European development finance—not a separate pot of additional aid.

Defining Characteristics of Global Gateway Camouflage Projects

Global Gateway camouflage projects are those GG initiatives that are publicly branded as having considerable benefit for partner countries, when in fact they are intended to cover up for more harmful extractive projects.

These projects, upon careful analysis, typically exhibit one or more of the following distinct characteristics:

Vagueness and Strategic Misalignment

They are often vaguely defined and lack clear, measurable outcomes, with little tangible clarity on how they concretely fit within the overarching joint EU-Africa 2030 Strategy. Examples: "Gender Transformative Action" in Tanzania, "Sustainable cocoa: from deforestation to reforestation" in Ivory Coast, while inherently laudable in isolation, are frequently merely repackaged versions of existing, traditional development aid, lacking the scale, innovation, or specificity required to be truly transformative.

Policy Conditioning

They are often explicitly or implicitly aimed at driving policy and regulatory change in partner countries, with the core objective of creating an "enabling environment" for European private sector entry and dominance in strategic areas like digital infrastructure, green energy, and raw material extraction. Example: BRT in Kenya, Vaccine initiative in Rwanda.

Lack of Additionality

They are either already under implementation under initiatives that predate the GG by many years, or they are projects of such a scale that they could have been easily funded by local national resources or traditional development grants. Examples: The Kariba Dam Rehabilitation Project in Zambia, for instance, was approved and funded by the EU as far back as 2017, four full years before the GG's grand inception. Similarly, the Mwache Water Project in Kenya received initial approval from the World Bank in 2013, with its later phases awkwardly and retroactively retrofitted into the GG portfolio to inflate its visibility.

Public Relations Facade

They are intentionally selected to be highly publicly visible and politically popular (e.g., school renovations, local feeder road rehabilitation, small health clinics) to generate immediate goodwill and media coverage, thereby strategically covering up for the more critical, geopolitically sensitive, and financially substantial projects focused exclusively on strategic resource and logistics corridors.

Double-Dipping and Obfuscated Funding

They are often projects already fully funded by other multilateral loans (e.g., from the World Bank or the African Development Bank) and do not represent new EU financial mobilization, thereby creating a deliberately misleading impression of scale, activity, and generosity.

Case Studies in Camouflage: A Closer Look

MAV+ in Rwanda

The "Manufacturing and Access to Vaccines, Medicines and Health technologies" (MAV+) initiative in Rwanda is a prime example of an inherently worthwhile project being strategically repackaged as a GG success story. However, as critically noted by MenaFEM in their incisive 2025 briefing, "Key concerns about the Global Gateway remain unaddressed," the initiative relies heavily on pre-allocated EU health budgets and the technical work of pre-existing European agencies like the European Medicines Agency. The "GG" label adds a powerful communications layer but contributes little new substantive capacity or groundbreaking funding, while simultaneously ensuring the resulting intellectual property and production partnerships primarily benefit established European pharmaceutical giants like BioNTech.

Kariba Dam Rehabilitation (Zambia/Zimbabwe)

This project stands as the quintessential example of a non-additional GG project. The EIB itself publicly lists its initial approval for the project funding in 2017. The essential rehabilitation work was a long-standing necessity for international dam safety and regional energy stability. Its deliberate inclusion in GG catalogues and promotional materials is a transparent attempt to artificially inflate the initiative's portfolio with projects that would have logically occurred with or without the Gateway's existence.

The Strategic Core: The Undisputed Priority of the Lobito Corridor

In stark and revealing contrast to these numerous camouflage projects, the Lobito Corridor project, a major infrastructure undertaking connecting the mineral-rich DRC and Zambian Copperbelt to the Angolan Atlantic port of Lobito, receives coordinated, high-level political support from the highest echelons of the EU and the US governments. A recent Financial Times article (October 2025) authoritatively highlighted the fierce geopolitical and economic competition surrounding this specific corridor, noting that the EU and US are openly racing to counter Chinese dominance in critical mineral supply chains. The GG investment here is undeniably strategic, sharply focused, and directly tied to European industrial security and competitive positioning. This single, high-profile corridor reveals the GG's true, unstated priority: securing the efficient and reliable flow of raw materials crucial for the European digital and green economy, not fostering balanced, inclusive, or continent-wide development based on locally-defined priorities.

Case studies in Selected Global Gateway Projects

The Lobito Corridor — Global Gateway's Core Extractive Route

Let us not kid ourselves. Look closely and you will see a close link between the Lobito Corridor and Europe's mapping of critical raw materials and other minerals. The key interest of the Lobito Corridor is to use it as a means of transporting minerals and materials from Angola, the DRC and Zambia all the way over to the EU and the US.

The Lobito Corridor, as opposed to other corridors, is not a straight-forward linking of various countries and economic regions that would like to pursue intra-country trade. Instead it is a meandering curve whose motive is anything but a corridor.

It is supposed to connect the Democratic Republic of Congo and Zambia to the Atlantic Ocean. The route will run through Angola to the port of Lobito.

The Lobito Corridor is conceptualized around a 1,300 km stretch of railway line from the port of Lobito, on the Angolan Atlantic Ocean coast, to the town of Luau on the north-eastern border of Angola with the DRC and within easy reach of north-western Zambia. The railway line extends a further 400 km into the DRC to the mining town of Kolwezi. The Corridor has recently been concessioned to a consortium comprising the commodity trader Trafigura (49.5%), and European partners Mota-Engil (49.5%) – construction, and Vecturis (1%) – railway operations.

Several MoUs and agreements focusing directly or indirectly on the development of the Lobito Corridor have recently been signed. Common among them is a sharp focus on the use of the Corridor as a route along which strategic minerals, CRMs, and EV battery value chain products can be transported to the EU and the US. For example, an MoU signed by the EU, the US, the DRC, Zambia, Angola, the African Development Bank (AfDB), and the Africa Finance Corporation (AFC) describes an extension of the railway line to Zambia. Meanwhile the Lobito Corridor Transit Transport Facilitation Agency Agreement (LCTTFA) – signed by the governments of Angola, the DRC, and Zambia – will accelerate domestic and cross-border trade along the Corridor and foster the participation of small and medium enterprises (SMEs) in value chains.

More recently, the EU has also signed specific MoUs with the DRC and Zambia. The latter, titled "Partnership on sustainable raw materials value chains", outlines how the EU is seeking to secure the supply of strategic minerals and CRMs.

In addition, the US has signed a tri-lateral MoU with both the DRC and Zambia supporting the development of a value chain in the Electric Vehicle (EV) battery sector. In this case, the US is very deliberate that it is about supporting the development of a value chain in the EV battery sector and commits to promoting the Zambia and DRC EV Battery initiative within the US private and investment sectors.

The International Energy Agency (IEA) has estimated that between 2020 and 2040, demand for nickel and cobalt will increase by twenty times, for graphite twenty-five times, and for lithium more than forty times. This projected surge in demand for CRMs has fuelled great interest in the Lobito Corridor, and with it an inevitable scramble for access. The DRC, as the world's largest producer of cobalt (estimates are consistently around 70% of global production), has found itself at the epicenter of this scramble, as has, by association, Zambia.

The EU and the US are among those vying for a place at the table, indicating that they will explore the development of green power projects and support investment in CRMs and clean energy supply chains along the Corridor. The awarding of the Lobito Corridor operation concession to the above-mentioned three-member consortium (comprising two European partners) has also added impetus to the renewed focus on the Corridor from the EU perspective.

To illustrate the EU's interest in creating 'highways for critical minerals' to secure its demand: the Lobito Corridor links the mining areas of Katanga province in the DRC — home to more than 50 per cent of the world's cobalt reserves — while also passing the Copperbelt in Zambia. International mining companies dominate these resource-rich regions.

The project was resuscitated in late 2023 under the United States Partnership for Global Infrastructure and Investment (PGII). US officials estimate costs of more than USD 1 billion, yet no public breakdown exists of concessional financing from donors including the EU, host-government contributions, or private finance to be mobilised. Global Gateway's involvement brings projects to G7-based investors and commercial partners such as CitiGroup, rather than fostering local value for host countries. Privatised infrastructure models that compel Global South citizens and governments to pay expensive user fees appear to offer not a development investment but an extractive rent.

The Energy Investment Ethiopia Does Not Need — Assela I Wind Farm

Owned by Ethiopian Electric Power (EEP), the Assela I Wind Project was fully financed by Denmark: a total investment of €146 million, supported by a €117.3 million Danske Bank loan and a €28.7 million grant. The project is expected to generate 300,000 MWh — enough for 400,000 households — and offset 260,000 tonnes of CO₂ a year.

Siemens Gamesa Renewable Energy was awarded the EPC contract (Danish subsidiary 60%, Spanish parent 40%) to install 29 turbines for €143 million. According to EEP CEO Ashebir Balcha, one condition of the loan agreement is to give the project exclusively to Danish companies. Supervision was awarded to Danish consultancy COWI after a closed bid that considered only Denmark-based firms (COWI and SWECO). Public debt on the Ethiopian side; tied procurement routing engineering and construction work back to European primes.

Nairobi Bus Rapid Transit

Core Bus Rapid Transit Line 3 (BRT 3) that will receive €347.6 million in subsidies, with most of these going to acquiring European electric buses managed by European technology and accessories on a 45km route when these resources are sufficient for 333km of excellent road network desperately needed in Kenya.

Meanwhile, the Kenyan treasury is preparing tax incentives to be submitted in the 2024 Finance Bill for lowering taxes and customs duties on "the importation, local assembly or marketing of electric vehicles". It is clear that the Nairobi Bus Rapid Transit has a much bigger political and market policy changes for the European corporations and the buses are just the first step to that direction. And it does not end there. Eventually, the project will link Nairobi to Kisangani, with one of the largest mineral resources in the DRC.